- The City Sponge

- Posts

- New Law: "Flooding Right To Know"

New Law: "Flooding Right To Know"

What renters, buyers, sellers in NYC should know on specific flooding questions.

The City Sponge “Flooding Right To Know” photo: Kenny Eliason

What’s going on in your basement?

If there is a little water down there, you are not alone. NYC is flooding more often. So in recognition that more water is coming AND that flooding may not be visible when people are looking for a place to live, the NY State government has enacted a new law known as “Flooding Risk Right To Know” which went into effect March 20, 2024.

The new law requires home sellers to disclose more detail specific to flooding issues at the property. It follows a similar law passed about 2 years ago for landlords and renters.

So today, if you are renting, buying, or selling a place in NYC, flooding now has to be one of the topics…by law.

FOR SELLERS / BUYERS:

Here are the specific flooding/water questions pulled from the new Property Disclosure Condition Statement (a state form filled out by the seller for the buyer):

Are there any flooding, drainage or grading problems that resulted in standing water on any portion of the property? If yes, state locations and explain…

Has the structure(s) experienced any water penetrations or damage due to seepage or natural flood event, such as heavy rainfall, coastal storm surge, tidal inundation or river overflow? If yes, explain…

Is there any rot or water damage to the structure or structures? If yes, explain…

Is any or all of the property located in a Federal Emergency Management Agency (FEMA) designated floodplain? If yes, explain…

Is any or all of the property located wholly or partially in the Special Flood Hazard Area (“100–year floodplain”) or a Moderate Risk Flood Hazard Area (“500-year floodplain”) according to the FEMA’s current flood insurance rate maps for your area? If yes, explain…

[ 😳 What does “100 /500 year floodplain”really mean? Scroll down👇 ]

Is the property subject to any requirement under federal law to obtain and maintain flood insurance on the property? If yes, explain…

Have you ever received assistance, or are you aware of any previous owners receiving assistance, from the Federal Emergency Management Agency (FEMA), the U.S. Small Business Administration (SBA), or any other federal disaster flood assistance for flood damage to the property? If yes, explain…

Have you ever filed a claim for flood damage to the property with any insurance provider, including the National Flood Insurance Program (NFIP)? If yes, explain…

Is there flood insurance on the property? If yes, attach a copy of the policy…

Is there a FEMA elevation certificate available for the property? If yes, attach a copy of the certificate…

[ Click here to see official NY State Property Disclosure Condition Statement.]

[ ⬇ More links below on on flood plain, elevation, insurance, templates. ]

FOR RENTERS / LANDLORDS:

The information required for renters from landlords is a bit less than the home seller, but still flood-specific. Examples below.

Has the leased premises has experienced flood damage due to a natural flood event, such as heavy rainfall, coastal storm surge, tidal inundation, or river overflow?

Are any or all of the Leased Premises is located wholly or partially in a Federal Emergency Management Agency (“FEMA”) designated floodplain?

Are any or all of the Leased Premises is located wholly or partially in the Special Flood Hazard Area (“100-year floodplain”) or a Moderate Risk Flood Hazard Area (“500-year floodplain”) according to FEMA’s current Flood Insurance Rate Maps for the leased premises’ area?

NOTICE TO TENANT: Flood insurance is generally available to renters through the Federal Emergency Management Agency’s (FEMA’s) National Flood Insurance Program (NFIP) to cover your personal property and contents in the event of a flood. Contact FEMA for rates. A standard renter’s insurance policy does not typically cover flood damage. You are encouraged to examine your policy to determine whether you are covered.

[ 😅 see our related piece on Flood Insurance ]

Q: So what is the biggest change in the most recent law (for sellers/ buyers)?

A: On flooding questions, a seller can no longer say “I don’t know” and pay $500.

There are two specific “Yes/No” questions that don’t allow for a vague answer. How much detail is required remains an interpretation, but because it is part of the “Property Condition Disclosure Statement” it is included as part of binding real estate contracts.

The previous $500 deduction was “loophole that allows sellers to pay $500 to avoid disclosing information about a property’s known flood history,” according to Kate Boicourt, New York-New Jersey Director of Climate Resilient Coasts and Watersheds for Environmental Defense Fund.

On the question of legal liabilities, the law is relatively new and still being interpreted, so the exact penalties or enforcement of this are not yet known.

But unlike before March 2024, a seller can no longer say “we didn’t know about flooding” and simply take $500 off the closing costs to cover themselves. The legal and financial liability have increased.

Did someone send you this? Please subscribe.

Q: If a landlord doesn’t disclose this information, what can happen?

A: The renter is more empowered.

We posed this question to Polina Rybachuk at AugRisk, a firm that specializes in disaster and societal risk factors in 50 states and has an eye to the specifics on this. She said that non-compliance with these new “Right To Know” flooding laws can lead to significant legal consequences for landlords, including:

Fines: Landlords may face monetary penalties.

Lease Termination: Tenants may be able to break their leases without penalty.

Civil Liability: Landlords could be held liable in civil court for actual flood-related damages due to non-disclosure.

To be helpful, Augurisk provided on request a sample updated lease developed by the NY State Office of Integrated Housing Management which incorporates the “Right To Know” information and can serve as a model to be used by building owners.

|

Q: How do I determine my floodplain AND if flood insurance required?

A: Look it up using your address.

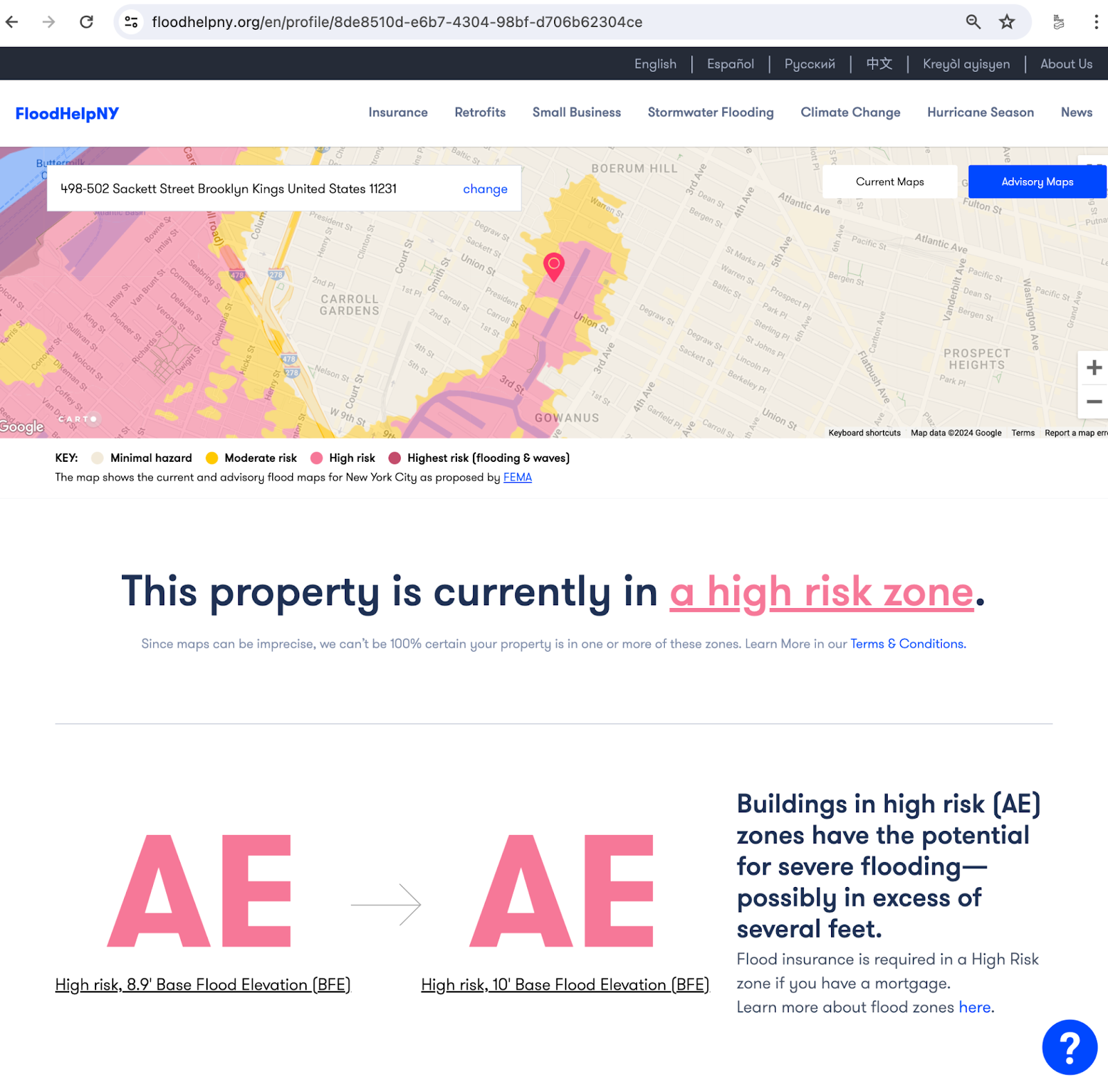

To answer the questions on floodplains and determine if flood insurance is require, go to FloodHelpNY which is a great web site to see the property’s flood zone risk by entering the address.

When you search up the address, it should look like a pin on a map with a listed flood plain designation AND IF Flood Insurance is required or not.

They also have a helpline: 646-786-0888.

Q: What is the deal with these terms: “100 / 500 year floodplain”?

A: Big topic…but the short answer is that is how they describe the probability of being flooded.

100 year: 1% chance of being inundated by a flood each year

500 year: 0.2% chance of being inundated by a flood each year

But as people in NYC can attest, floods are happening more often than that, so it really it is just an indicator of more or less flooding potential.

Source: FEMA

Note: There is a lot of talk about changing this terminology because “100 year” storms seem to happen every few years now. More here if interested: https://fivethirtyeight.com/features/its-time-to-ditch-the-concept-of-100-year-floods/

Q: If I’m considering a short 1-2 year lease, or plan on selling the place within 20 years, why should I care about being in a “100 or 500 year” floodplain?

A: Because that area will flood more often.

Intense cloudburst storms are increasing and flooding happening every year and sometimes multiple times a year, especially with storm surges on coastlines which really affect NYC which has 520 miles of coastline. This is especially important if you plan to live in basement apartments…11 people have drowned in NYC basement apartments in recent years.

Q: I can see how this would cost me money, but how would it save or make me money?

A: It does cost some now…but saves more. You also increase safety, reduce legal risk and getting dinged on price reduction. Lastly, flood insurance reimburses for some mitigation work.

Flood loss is more expensive than flood prevention.

Some stats: In 2021 in New York State, 7,645 homes were purchased that were estimated to have been previously flooded according to an NRDC report. It goes on to say: “the average home in New York State with prior flood damage has an expected average annual loss of $3,126, compared to $93 for the average home. Over the course of a 15-year mortgage, average expected damages to the previously flooded home equate to $46,887 (in today’s dollars); for a 30-year mortgage flood damages equate to $93,774.”

Federally-backed flood insurance - required for certain areas but recommended for more - reimburses up to $1,000 for certain mitigation materials/labor (see our related piece on Flood Insurance).

Low-lying apartments really need this: it is estimated that there are over 4,000 NYC basement apartments in a flooding “high risk area,” according to the New York Federal Reserve Bank Liberty Street Economic report. Before you rent or buy down there, KNOWING if you will need to retrofit, build better, purchase flood insurance - or even evacuate ahead of a major storm must now be disclosed.

Q: Will this help or hurt home owners and landlords?

A: It should bring a sense of relief to renters, buyers AND sellers while rewarding people for doing the right thing.

POV of one home seller: We spoke to one homeowner who recently sold their Brooklyn home and had been concerned about how to discuss a history of flooding, which had happened on a handful of occasions during extreme rainfall events.

Their lawyer, who was still trying to determine how to interpret the new law, advised: just tell the truth.

The home owner said after the form had been approved by their lawyer and submitted to the buyer, there was a real sense of relief. They had wanted to do the right thing, although they didn’t want to jeopardize the sale - but with the form honestly representing the property’s flooding history they now didn’t need to worry about any legal risk after closing.

So instead of a back and forth debate on how much to share, they just shared it, with a short description in the Disclosure Statement.

The reaction? The owner told me that these buyers stated they knew that a lot of homes have these issues in Brooklyn and it’s just part of living in this neighborhood - and so the disclosure was accepted without further issue or discussion.

So in this case, the new law informed the buyer, but also made the seller feel significantly less anxious about the transaction.

Q: I don’t want to spend money, so can I just wait for the city to fix the sewers?

A: You can, but since you have to disclose, better to not wait and hope (and lose $ and value).

Waiting for the city gov’t or the DEP to solve all the flooding issues on your street isn’t a viable strategy. They are already working on many big projects in priority areas but honestly many will take 2-10 years to see some of benefits (see related story What 1 Inch of Rain Can Do).

Since you now need to document your flooding history, it would be good to also explain any steps you are taking to address it.

By owners acknowledging the flooding realities and taking mitigation steps, you can win trust from people and ultimately save / make money with your “flood smart” property.

Q: I’m a seller / buyer: how do I determine the property elevation?

A: You can get new one or update the existing one.

An elevation certificate may be required depending on where your property is (again find your zone, per above). This may also be useful in lowering flood insurance.

You can find elevation certificate general info with regard to flooding insurance here: https://www.floodhelpny.org/en/elevation-certificates

You can also use an existing elevation certificate and update it to lower your premiums. To update existing elevation certificates, here is the state form: https://www.nyc.gov/assets/housingrecovery/downloads/pdf/2019/how_to_update_your_elevation_certificate_v20190424.pdf

Q: So if there is a flood risk and I still want the place, what do I do?

A: Now that you know, you can be smarter.

If you are a renter, confirm what the landlord will cover if flooding occurs. Per National Flood Insurance Program, the landlord is responsible for the building needs/damages, but YOU will be responsible for your possessions (and yes there is flood insurance for renters). If it is a basement apartment, ask about what happens to the drains, toilets, and sinks during a flood and what measures are in place to stop back flow. Lastly, confirm you can get out safely if a flood is extreme.

If you are a buyer, understand the flood history of the place (as now required by law) AND the street, and see what mitigation approaches are already in place or might need to be added. Ideally you can talk to some neighbors on the street and let them share their experiences about flooding. Then use that information and potential costs in your decisions.

Q: What are the actual laws and language?

A: Here.

Law for landlords / renters: “Real Property (RPP) CHAPTER 50, ARTICLE 7, Section 231-B Senate Bill 21335”, passed in Dec 2022.

Law for home sellers / home buyers: “Real Property Law Amd §§462 & 465, rpld §467, RP L, Senate Bill 24500”, passed in June 2023.

Who was behind these laws:

State Senator Brad Hoylman-Sigal (Manhattan West Side)

State Senator Shelley B. Mayer (New Rochelle, White Plains)

Assembly Member Robert Carroll (Park Slope, Kensington, BK Heights)

Assembly Member Steven Otis (Portchester, Rye, Mamaroneck)

Waterfront Alliance as part of their Rise2Resilience platform

Other helpful sites on this topic:

General flood info help site for residents and small businesses, including flood risk maps by specific location but also good Q&A section.

Gov’t page on rights and free legal options.

A private company specializing in “disaster and societal risk factors in 50 states” who I found that does a great job explaining how building owners can comply and offers that as a service…seems it might be more landlords.

See the new updated PCDS template for home sellersand buyers with new “Right To Know” law and questions.

These laws were part of broader set of policies they advocate for in NY State and the comprehensive needs to prepare for more water/flooding.

If you read to the bottom, that’s good! Please share with others.

Have an idea for a story we should do or read? Let us know.

Reply